New Agent-native business validation workspace

From messy folders to repeatable AI-assisted workflows.

HypoGrid is a local-first, agent-native workspace that helps builders and investors design, run, and review business validation workflows — without outsourcing judgment to AI.

Built for validation workflows across

Agent-assisted business validation, human judgment at every gate.

Built to compress the slowest parts of hypothesis testing: source review, assumption framing, evidence mapping, contradiction finding, and decision capture.

- Manual validation assembly

- 0 Designed to reduce the hours spent turning raw notes, interviews, research, and AI outputs into a traceable validation record.

- Validation playbook sources

- 0 A curated reference base of venture essays, operator playbooks, customer discovery methods, and market research heuristics that informs the workflow.

- Validation methods

- 0 Market sizing, customer segmentation, interview synthesis, competitive landscape, GTM quality, pricing, unit economics, and more.

- Workflow templates

- 0 Reusable validation flows for new business discovery, startup diligence, customer interviews, market research, red-team review, and decision memos.

Why not spreadsheets or Notion?

LLMs accelerate research and analysis.HypoGrid makes better judgment repeatable.

Use spreadsheets, Notion, and AI chats as inputs. HypoGrid keeps the hypothesis at the center, connecting evidence, contradictions, open questions, and human-approved decisions into a learning loop.

01 — Core methodology

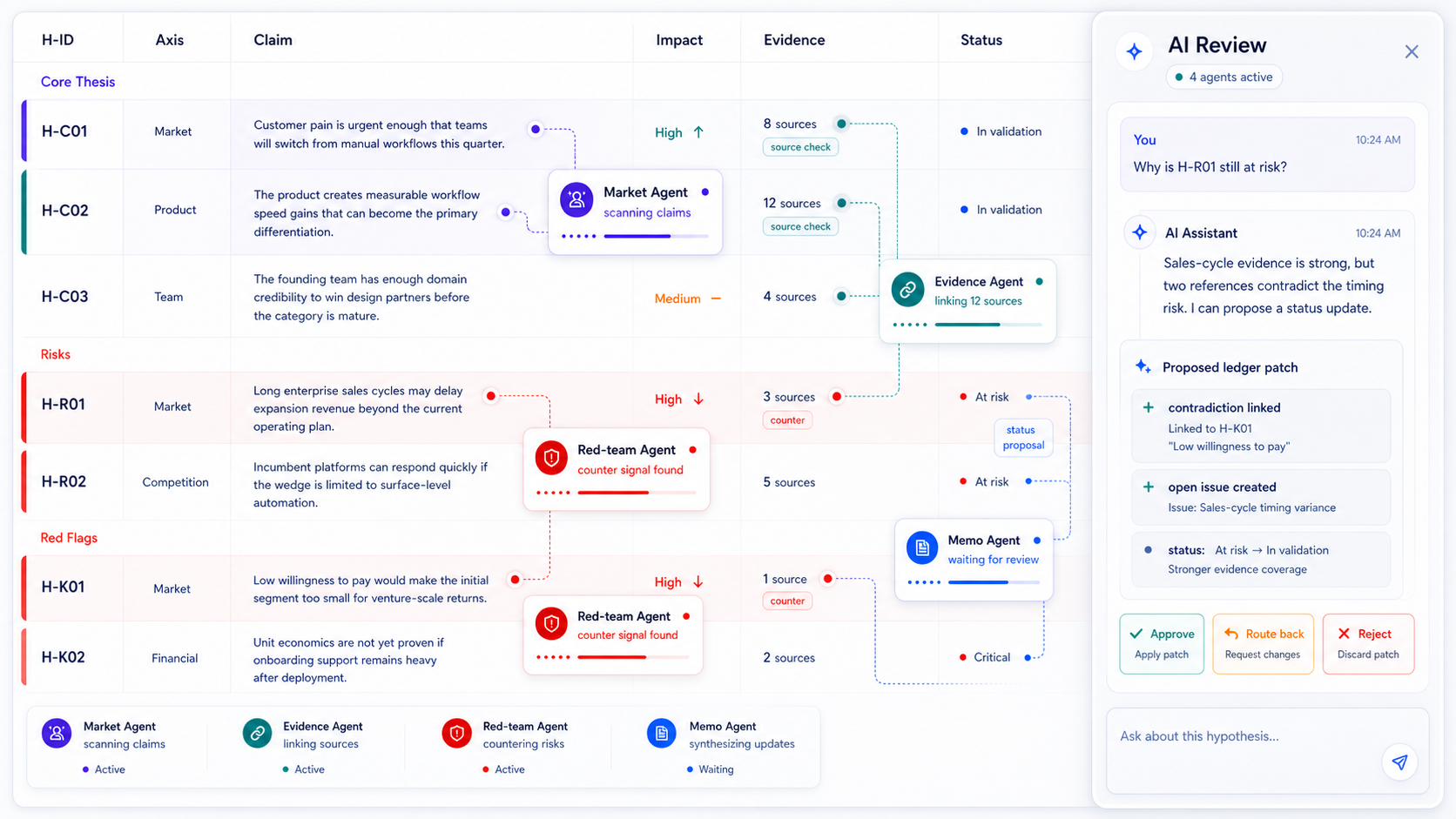

The unit of work is a hypothesis, not a section.

Every hypothesis becomes a living object. Evidence, contradictions, new information, critiques, and decisions keep updating it as the work moves. Instead of collecting notes, HypoGrid helps teams test, update, and decide against hypotheses.

02 — Product proof

See which assumptions are holding,breaking, or ready for agent support.

HypoGrid gives teams multiple views of the same validation record while AI agents help scan claims, link sources, surface contradictions, and propose human-reviewable patches.

Human in the loop. Closed-loop learning.

Human judgment turns AI execution into compounding learning.

HypoGrid runs a human-in-the-loop cycle for record changes and a closed-loop learning cycle for reuse. Agents scan and propose, people approve what advances the record, and each approved decision becomes context for the next company, market, or initiative.

03 — Use cases

For teams that need to pressure-test business assumptions.

VC, CVC, and deal teams

- Turn post-screen diligence into hypotheses, evidence, contradictions, and explicit open questions

- Keep dataroom materials, public research, and call notes attached to the claims they support or challenge

- Generate memo drafts from human-approved claims instead of rewriting scattered notes from scratch

- Preserve why the team moved forward, routed back, tracked, passed, or pursued a term sheet

Founders and new-business teams

- Decompose new ideas into testable propositions before teams overbuild around weak assumptions

- Attach customer interviews, prototype metrics, and market signals to the assumptions they test

- Use critique loops to argue against your own plan before an investor, executive, or board does

- Walk into reviews with a clearer answer to what is known, believed, contradicted, and still unknown

04 — Technology stack

Local-first infrastructure for auditable AI-assisted workflows.

HypoGrid is designed for sensitive validation work: materials can stay inside the user's trust boundary while workflows, ledgers, agents, and outputs stay structured.

Local Forest Trust Boundary

Use a local folder as the workspace. Store paths, metadata, and projections in SQLite while source materials remain in the user's file system.

Configurable Workflow

Point HypoGrid at prior diligence or validation folders, extract the pattern of work, and turn it into a repeatable process the team can tune.

Multi-Agent Orchestrator

Analysis packs for startup DD, commercial DD, financial DD, founder DD, expert interviews, and other validation workflows can run in parallel.

Ledger Layer

Hypotheses, evidence, contradictions, open issues, and decisions are tracked with stable IDs so every view and report renders from the same record.

05 — Built-in Agents

Compose agents into practical validation workflows.

Combine built-in agents to create repeatable workflows for diligence, market research, customer discovery, red-team review, and memo preparation. Teams can rename, tune, and sequence agents around the way they actually validate decisions.

Seed lead investment DD

Turn a founder deck, dataroom, calls, and market notes into core thesis, risks, red flags, and IC-ready questions.

Fintech market entry research

Compare segments, competitors, regulation, pricing, and timing signals before committing to a new wedge.

B2B SaaS new-business discovery

Decompose a new product idea into assumptions, customer segments, validation tasks, and decision gates.

Interview evidence mapping

Extract pull signals, objections, contradiction patterns, and follow-up questions from customer interviews.

Commercial DD challenge pass

Stress-test GTM repeatability, customer concentration, churn risk, and the assumptions most likely to break.

Composable validation workflows

Founder DD, pricing tests, cap table review, comps, sector thesis, memo prep, portfolio strategy, and more.

Private beta

Request private beta access.

HypoGrid is still early and onboarding is handled personally. If you are exploring hypothesis-led diligence for a fund, CVC team, or company-building workflow, send a short note on X.

Built by

Entrepreneurial investor and former founder building HypoGrid. After 10 years across startups, company building, and venture investing, I am turning the messy work of hypothesis-driven diligence into a closed-loop, auditable workflow that keeps learning and getting sharper. If your team is actively pressure-testing companies, I would love to hear where the product should go next.

Turn pattern-match into structure.

HypoGrid is opening private beta access for venture teams and company builders who want a more auditable way to reach conviction.